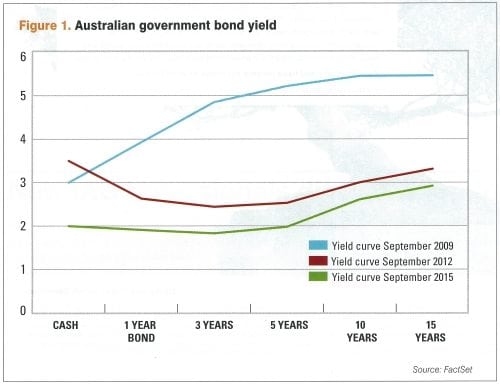

Local equities down but so are the others

The Australian equity market suffered its worst third quarter this year since the same quarter in 2011.

The All Ordinaries index dropped by 7.2% in the September quarter, taking its overall performance down 6.1% in the first nine months of 2015. Below-trend growth in the domestic economy or more worryingly, predictions of a recession — and its nasty consequences for corporate profits — has soured investor appetite for the local bourse.

“[The risk of recession] currently stands at the greatest probability since the global financial crisis”, the Sydney Morning Herald printed on 11 September quoting GS chief economist Tim Toohey.

This was quickly followed by Kima Capital’s warning that, “Australia is destined for a difficult recession at worst or a prolonged period of well-below-trend growth at best” again printed in the SMH less than three weeks later.

With such dire predictions, the Australian equity market’s negative return so far this year is hardly surprising.

However, the local bourse is caught in the same headwinds that are buffeting all other quity markets worldwide. THe All Ord’s minus 6.1% return is less than a percent lower than the negative 5.4% from developed market equities and better than the negative 9% return from emerging market equities over the same period.

To be sure, this would not prevent the Australian economy from succumbing to a recession but recent economic data and survey updates indicate it’s improving. — resilient, at worst — despite the on-going slow growth in the global economy and slowdown in emerging economies.

For instance, the latest NAB business survey shows confidence reviving to a plus 5 reading in September from plus 1 in the previous month. While the change in leadership from Abbott to Turnbull could have boosted confidence, remember that September was not a particularly good month due to heightened financial market volatility that culminated in the worst September quarter for equities since the third quarter of 2011.

This gives credence to NAB’s assessment that, “Overall, the business survey suggests a good degree of resilience in what appears to be a building non-mining sector recovery.” More so given the business conditions index remains elevated at a plus 9 reading, unchanged from August but up from the plus 6 reading in July.

Consumer confidence has also recovered. The Westpac/Melbourne Institute index of consumer sentiment rose by 4.2% to 97.8 in October from 93.9 in September. While still below 100 (optimists outnumber pessimists), the components of the index showed sharp improvements: Economic conditions expectations soared by 20% over the month, unemployment expectations dropped by 16.3% and expectations for family finances increased by 3.5%.

[via Financial Standard]